Exporting goods and own products outside of Russia is a financially profitable operation for taxpayers. The legislation provides for a special procedure for calculating and refunding value added tax (VAT) for enterprises involved in export activities:

- the VAT rate on goods/services shipped for export is set at 0%;

- tax paid on the purchase of products intended for export abroad is subject to reimbursement from the state budget.

Due to the need to return from the budget VAT paid on Russian territory, fiscal authorities pay special attention to enterprises that use export operations. An unreasonably claimed VAT refund or failure to comply with the regulations for confirming the right to apply a preferential tax rate is fraught with substantial additional payments to the budget and penalties.

VAT rate for export

There are several points of view explaining the appearance of the 0% VAT rate.

On the one hand, VAT is an indirect tax paid by the buyer. Foreign buyers are not subject to the Russian Tax Code and therefore do not have to pay Russian VAT. In this regard, the sale of Russian goods and services to foreigners should occur without tax.

On the other hand, exports are of great importance for the economic growth of the country, so the state is interested in businesses striving to develop sales not only within the country, but also abroad. To increase the interest of entrepreneurs in export operations, there are various stimulating economic instruments. One of them is the VAT rate for export transactions, equal to 0%. Against the backdrop of fairly high regular VAT rates, one of which was recently increased, the use of a zero VAT rate for exports looks very attractive.

Let us remind you what VAT rates exist in Russia in 2021:

Shipment of goods by a Russian supplier from abroad

Let's imagine the situation. A Russian manufacturer sells its products to a foreign partner. In this case, the manufacturing plant is located on the territory of a third state, from where the shipment is made, bypassing Russian territory. Is this an export or not, and what about VAT?

The law says the following. We can talk about the emergence of an object subject to VAT only when it is sold on the territory of the Russian Federation. Russia is recognized as a place of sale only if the goods were on its territory at the time of shipment or transportation. In the case under consideration, the Russian Federation is not the place of sale and, therefore, there can be no talk of any VAT or its reimbursement.

Zero rate

So, the subject of our article is VAT on the export of goods.

As mentioned, the VAT rate for exports is 0. Clause 7 of Art. 164 of the Tax Code of the Russian Federation was introduced recently and allows in some situations to refuse the 0% rate:

It is logical to ask, for what purpose or for what reasons can one refuse a preferential rate? One of the reasons is this: you cannot simply take and apply a 0 VAT rate when exporting; you need to confirm it. And confirmation of the 0 VAT rate for export requires the collection of a large amount of documentation, that is, labor and time costs.

We will tell you further what is needed to confirm the zero VAT rate for export.

Confirmation of eligibility for a 0 percent rate

The procedure for confirming the zero VAT rate is described in Art.

165 Tax Code of the Russian Federation. To prove the legality of applying the zero VAT rate for exports, it is necessary to generate the following package of documents:

Instead of copies of the specified documents, paragraph 15 of Art. 165 of the Tax Code of the Russian Federation allows the submission of electronic registers indicating the registration numbers of the relevant declarations.

Electronic registers must be compiled in approved formats and sent to the tax authority via TKS through an EDI operator duly registered in the Russian Federation.

It must be borne in mind that during the audit, tax authorities may require the submission of documents from the electronic register.

The taxpayer is given 180 calendar days to collect documents.

If after 180 days the documents are not collected, the goods sold must be subject to VAT according to Russian rules (at the rates from paragraphs 2 and 3 of Article 164 of the Tax Code of the Russian Federation). If the taxpayer nevertheless collects the entire package of documents after 180 days and pays VAT under Art. 164 of the Tax Code of the Russian Federation, the right to submit documents to the tax office is retained. If the tax authorities come to the conclusion that the 0% rate has become confirmed, the previously paid VAT on exports will be returned to the taxpayer.

Clause 10 of Art. 165 of the Tax Code of the Russian Federation states that the VAT declaration and confirmation documents must be submitted to the tax office at the same time.

When can an exporter receive budget money?

Upon completion of a three-month desk audit, the tax service makes a decision in which it orders the exporting company to fully or partially reimburse the “input” VAT paid. The law allocates the supervisory authority no more than 7 calendar days to make a decision.

The taxpayer may declare his intention to use the refund amount to cover the existing arrears on mandatory payments. If such an application is not received by the Federal Tax Service, the compensation amount must be received in the exporter’s current account within five banking days.

Features of VAT accounting in the presence of export operations

If a company begins to export, then the question arises: what accounting features exist for this type of activity?

Let's analyze the subtleties of export in terms of VAT calculation. Let's consider the concept of export in relation to goods. When exporting services, VAT is paid in the general manner if they are provided on the territory of the Russian Federation. Services are not subject to VAT if provided outside the Russian Federation.

If an organization carries out both taxable and non-VAT-taxable transactions, then clause 4 of Art. 149 of the Tax Code of the Russian Federation requires separate accounting of such transactions, because one of the main conditions for accepting input VAT from a supplier for deduction is the condition that the purchased goods (work, service) are used for operations subject to VAT.

By analogy, we can say that when a 0% rate is applied, it becomes necessary to keep separate records of such transactions. Thus, separate accounting for VAT on exports is necessary.

Let's turn to the regulatory framework. Paragraph 3 clause 10 art. 165 of the Tax Code of the Russian Federation prescribes separate VAT accounting according to the rules established by the taxpayer himself, if he has activities taxed at a 0% rate. However, there is an exception to this rule: when exporting non-commodity goods registered after 07/01/2016, separate accounting can be omitted and VAT can be deducted in the general manner.

Deadline for determining the tax base:

Taxpayers using the simplified tax system, in accordance with paragraph 2 of Art. 346.11 of the Tax Code of the Russian Federation, must pay VAT when importing goods into the customs territory of the Russian Federation. However, nothing is said about the need to pay VAT on exports. Thus, when exporting, simplifiers do not have any VAT obligations.

Deduction for export transactions

A pressing question is whether an organization is entitled to deduct VAT when exporting?

The answer is yes. Input VAT for export, that is, the VAT that you paid to the seller for goods used for export, is deductible. But for this there is a certain procedure, somewhat different from the general procedure for accepting VAT for deduction. Those involved in the distribution of VAT on exports need to pay special attention to the process of VAT deduction.

The procedure for applying deductions when calculating export tax is described in paragraph 3 of Art. 172 of the Tax Code of the Russian Federation. It states that exporters of non-commodity goods can deduct input VAT in the general manner, that is, in the same way as for ordinary non-export sales. These rules were introduced on July 1, 2016. Those exporters who refused to use the preferential rate do the same.

For commodity exporters, the process of applying deductions depends on whether a package of documents confirming the zero rate has been collected or not. In addition, if VAT was accepted for deduction earlier, VAT restoration will be required when exporting this product.

What consequences may there be for the Russian counterparty?

If a company provides services to a Russian counterparty, for example, international transportation services, then both parties have a risk if the 20% VAT rate is illegally used.

A Russian counterparty can claim a VAT tax deduction based on the received invoice. But the document will not meet the requirements of paragraphs. 10 and 11 clause 5 art. 169 of the Tax Code of the Russian Federation, since it will indicate the incorrect VAT rate. Accordingly, the counterparty will not be able to receive a VAT deduction.

The Ministry of Finance clarified this point in its Letter dated 02/05/2019 No. 03-07-08/6650. This opinion of officials is also supported by the courts.

Filling out a VAT return when exporting

Let's consider what data and in what sections must be entered when filling out a VAT return for export.

Declaration for export of non-commodity goods

When exporting non-commodity goods, VAT is deductible according to the same rules as for ordinary transactions.

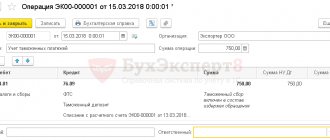

Line 120 of Section 3 must be completed. The fact that the collection of documents does not affect the period for recognition of the deduction does not exempt the taxpayer from collecting a package of documents confirming the zero rate. If this package is formed in the reporting quarter of shipment, the amount of the tax base falls into line 020 of section 4, and line 030 remains empty, otherwise a double deduction will result. Section 4 is completed in the same way during the period of receiving the full package of documents. An example of filling out a declaration regarding export, that is, filling out the specified lines, is shown below.

How to report VAT if you export raw materials

As already mentioned, when exporting raw materials the situation is different, which is why the declaration is filled out differently. For such exporters, there are special export sections 4, 5 and 6 in the declaration.

The completed sections of the declaration (they may be in different declarations for different tax periods) are presented below:

VAT refund on export

VAT refund when exporting is a frequent procedure.

This is due to the peculiarities of export operations, namely the fact that when a 0% rate is applied, the VAT charged to the buyer is zero. Provided that goods for export are purchased from VAT payers, that is, when input VAT exists, VAT refund on export becomes inevitable. The same situation as with the return of export VAT may arise for ordinary transactions carried out within the country. The procedure for refunding export VAT and regular VAT does not differ in any way. Only the package of necessary documents differs: as already mentioned, in order to receive a VAT refund when exporting from Russia, you must collect documents confirming the zero tax rate.

Differences between exports to the EAEU and other countries

Many Russian companies work with neighboring countries, so questions often arise about the specifics of paying VAT when exporting to Uzbekistan from Russia or about VAT reimbursement when exporting to Kazakhstan.

Peculiarities of trade in terms of VAT with close neighbors do exist, but not with all of them. Countries that are part of the Eurasian Economic Union (EAEU) are subject to special conditions:

So, what are the features of accounting for VAT when exporting to Belarus and other EAEU countries?

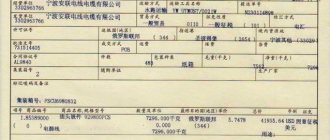

Despite the fact that VAT for exports to Kazakhstan and other EAEU states is zero, since in any case a zero tax rate is applied, an invoice must be drawn up. Indication of the zero VAT rate and the code of the type of goods according to the Commodity Nomenclature of Foreign Economic Activity is mandatory. Here is an example of filling out an invoice indicating the zero VAT rate when exporting to Belarus in 2021:

Bottom line

The most profitable VAT refund procedure is for large companies that regularly export goods in large volumes. In this case, professional work of a lawyer or customs broker is required. They should be aware of all the latest changes in legislation and have extensive experience in preparing customs declarations, and in some cases be ready to defend your rights in court.

You can independently and most fully familiarize yourself with all the intricacies of the VAT refund procedure in Article 165 of the Tax Code of the Russian Federation.